Build a DCF Model for Negative Earnings Startups

When a company is burning cash, the standard DCF template — discount projected earnings, subtract net debt, divide by shares — produces a number that looks plausible and a process that is fundamentally compromised.

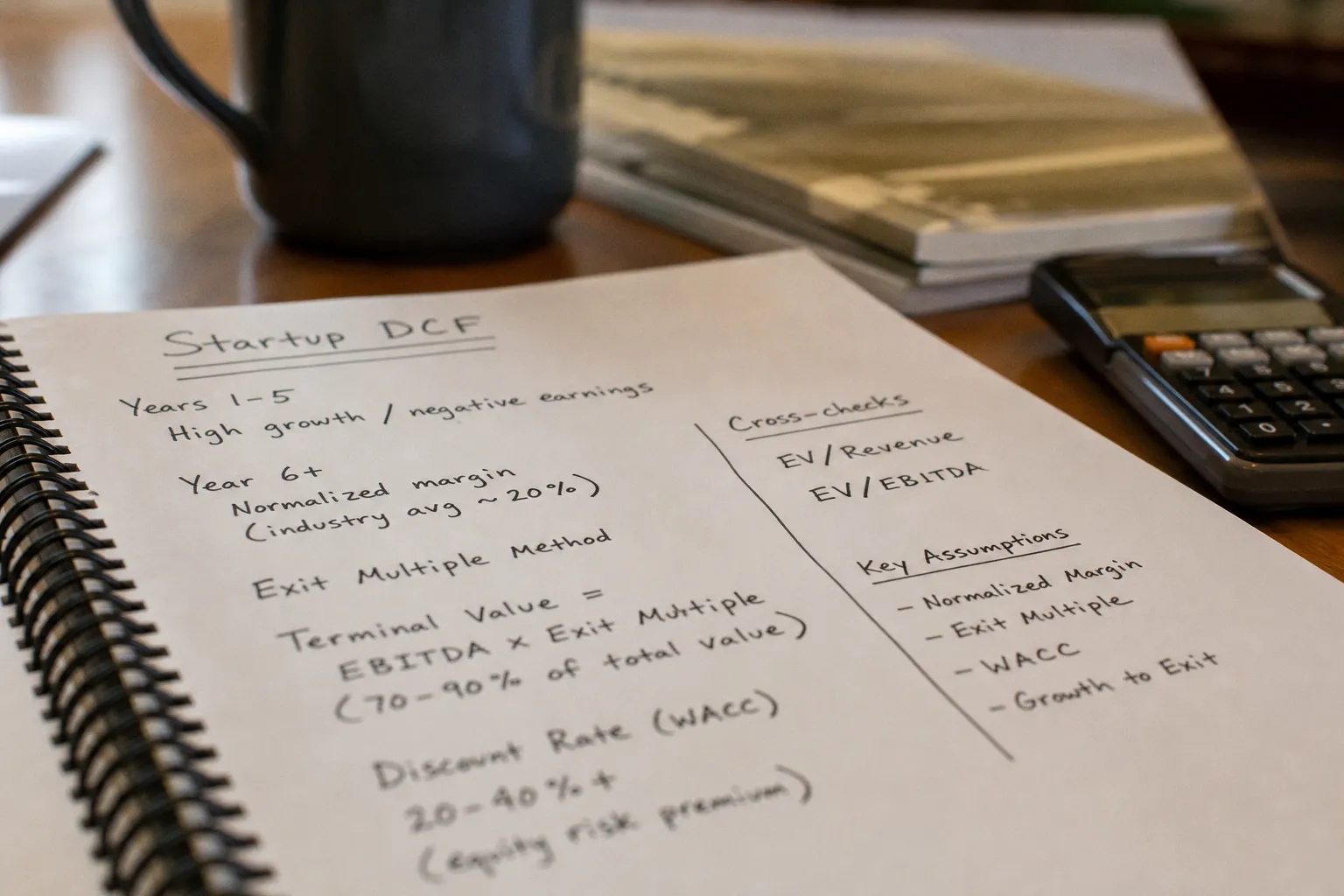

This is uncomfortable for analysts trained on stable, profitable businesses, where terminal value usually sits between 50 and 65 percent of the total. Push that contribution to 80 or 90 percent and you are not refining a number — you are manufacturing one. The modeler's responsibility shifts from producing a price target to controlling the variance inside the terminal block, documenting every constraint, and presenting the output as a range calibrated to explicit probability assumptions. The mechanics of how to build a DCF model for negative earnings startups have to be rebuilt from first principles, because the standard income-statement shortcut no longer applies.

Adjusting the Discount Rate for Startup Risk Profiles

The Weighted Average Cost of Capital is the single most important constraint you set, and for negative-earnings startups it sits well above the 7 to 10 percent range used for mature public companies. Our working band is 20 to 40 percent, calibrated to the stage of the company, its revenue trajectory, and the implied probability that it never reaches free cash flow positive.

For related context, see Long-read explainers and analysis: explainers, in-depth analysis, backgrounders, data.

For related context, see Q2 Earnings Season Nears Kickoff: Bank Earnings in Focus.

If the company is pre-revenue at Seed, we anchor near 35 to 40 percent. If it has shipped a product, signed enterprise contracts, and is at Series B with a clear path to gross margin expansion, 22 to 28 percent is defensible. The discount rate is not a single input — it is a function of three components that each require their own justification:

- Probability of full loss — the chance the company fails before generating sustainable free cash flow. We model this from stage-conversion data: historically, roughly 60 to 70 percent of Seed-stage companies fail before Series A, and the cumulative failure rate through Series C sits around 40 to 50 percent. That probability feeds directly into the discount rate as a survival-weighted adjustment. A company with a 30 percent chance of total failure needs its expected cash flows discounted at a rate that prices that risk in — not a generic "startup premium" bolted onto a CAPM output.

- Equity risk premium over the risk-free rate — standard CAPM logic, but with a beta that reflects the venture-stage return profile rather than the sector beta of a mature firm. Public-market SaaS betas cluster around 1.1 to 1.4; early-stage equity behaves more like a deep out-of-the-money call option, with return distributions that are heavily right-skewed. We typically apply a size premium and an illiquidity premium on top of the equity risk premium to capture this.

- Capital structure overhang — most early-stage companies are equity-funded, so WACC collapses to cost of equity. Convertible notes and SAFEs complicate this: the conversion terms create future dilution that is economically real but invisible in a simple equity-only model. We model the dilution scenario explicitly — what the fully diluted share count looks like at each funding round — and apply the discount rate to that expanded base.

The core discipline is parameter transparency. If a reader cannot trace how you arrived at 32 percent, the model fails the audit test regardless of what number it produces.

A DCF for a negative-earnings startup is not a pricing tool. It is a constraint engine that shows which assumptions must hold for the price to make sense.

Normalizing Operating Margins to Forecast Future Cash Flows

The explicit forecast period — typically five to ten years — requires projecting Free Cash Flow from a starting point of negative operating income. The standard approach is to select a "normalized" steady-state operating margin and then build a path from current losses to that margin over the forecast horizon.

The normalization anchor is not the startup's own history. It is the margin profile of mature peers operating in the same vertical at scale. If we are modeling a vertical SaaS company currently running at -40 percent EBITDA margin, we study public SaaS comparables that have reached steady state — typically 25 to 35 percent EBITDA margin for the survivors — and treat that range as the asymptote the FCF curve approaches by year seven or eight. The company's own track record tells us where it is today; the comparable set tells us where it can plausibly arrive.

The mechanics follow a specific sequence:

1. Build the revenue ramp from current ARR, observed growth rate, and unit economics. If the company has $8M ARR growing at 80 percent with net revenue retention above 120 percent, the top-line projection is constrained by those figures and by the growth decay rate as the base expands. No company in history has sustained 80 percent growth for ten years — the model needs an explicit decay schedule that reflects how growth moderates with scale.

2. Apply gross margin based on the cost structure — COGS as a percentage of revenue, hosted infrastructure costs, payment processing, customer support headcount. Early-stage gross margins often sit at 50 to 65 percent and expand toward 70 to 80 percent as the product matures and the cost base scales more slowly than revenue. The margin expansion curve itself should be modeled, not assumed to jump at a single inflection point.

3. Layer operating expenses as a percentage of revenue, declining with scale. Sales and marketing typically compress fastest as the brand develops and self-serve channels mature. R&D spending holds longer because the product still requires significant engineering investment. G&A compresses last, driven by finance, legal, and administrative overhead spreading across a larger revenue base.

4. Identify the EBITDA crossover year — the point at which operating income turns positive — and project forward at the normalized margin from that year onward. This crossover year is one of the most consequential assumptions in the model; shifting it by twelve months changes the present value of the entire cash flow stream.

5. Convert EBITDA to Free Cash Flow by adjusting for cash taxes, capital expenditure as a percentage of revenue, and changes in working capital. Early-stage companies often have minimal capex but significant working capital swings from annual contract prepayments and lengthening receivables cycles as they move upmarket.

The output is a U-shaped FCF trajectory: deep negative in years one through three, recovering toward zero by year five, and positive at scale in years six through ten. If the company never crosses zero within the forecast window, the entire intrinsic value is loaded into Terminal Value, and the assumptions in step 5 become the only thing separating a defensible model from a fantasy.

The Case for Exit Multiples Over Gordon Growth in Early-Stage Modeling

The Gordon Growth Model — Terminal Value = FCF × (1 + g) / (WACC - g) — assumes a stable, perpetual growth rate. For an early-stage company, that assumption is broken in three places simultaneously: the growth rate is too high to be perpetual, the cash flows are not yet normalized to a steady state, and the company may not survive long enough to reach the terminal year.

We use the Exit Multiple Method instead. Terminal Value is calculated by applying a target EV/Revenue or EV/EBITDA multiple to the terminal-year financials — typically year seven or year ten — and discounting that exit value back to today.

| Parameter | Gordon Growth | Exit Multiple |

|---|---|---|

| Required inputs | Perpetual growth rate g, normalized FCF | Forward multiple, terminal-year revenue or EBITDA |

| Implicit assumption | Company survives forever at stable growth | Company reaches a defined exit event or maturity milestone |

| Sensitivity profile | Hyper-sensitive to small changes in g or WACC | Constrained by observable peer multiples |

| Applicability to pre-profit | Poor — assumes stable cash flows that do not yet exist | Strong — peers in the same vertical provide benchmarks |

| Failure mode | Outputs explode when WACC approaches g | Outputs converge when peers trade in a tight range |

| Discipline test | Growth rate must be defended as perpetual | Multiple must be defended as below current peer trading |

The exit multiple should be sourced from comparable public companies at the same stage of maturity the startup is projected to reach at the terminal year. If the startup's year-seven profile resembles a mid-cap SaaS firm trading at 6x EV/Revenue, that is the anchor. We deliberately discount current public multiples by 1 to 2 turns to account for compression as companies scale — a 10x revenue multiple that looks reasonable for a hyper-growth company today can be aggressive for the same company at maturity.

The choice between EV/Revenue and EV/EBITDA as the terminal metric depends on where the company sits at the terminal year. If EBITDA is still thin or volatile, EV/Revenue is more stable and less susceptible to margin manipulation. Once margins have normalized and stabilized, EV/EBITDA captures operating efficiency more precisely. We select whichever metric produces the more conservative output and document the choice explicitly — it is one of the assumptions a reader should be able to challenge.

Managing the Terminal Value Dominance in Valuation Outputs

When terminal value contributes 70 to 90 percent of intrinsic value, sensitivity analysis is not a supplementary exhibit — it is the primary output of the model. The base-case DCF number is the least useful number the model produces. What matters is the range of outcomes across plausible parameter combinations.

We run the model across a structured parameter grid:

- WACC: ± 5 percentage points around the base case

- Terminal-year revenue: ± 30 percent

- Normalized EBITDA margin: ± 10 percentage points

- Exit multiple: ± 2 turns

The result is a valuation range. If the range spans $400M to $1.2B against a current implied valuation of $900M, the model tells us the price is plausible but dependent on a specific slice of the assumption space. If the range spans $50M to $2B, the model is telling us the inputs are too uncertain to anchor an investment decision — and the honest conclusion is to walk away or wait for more data.

We then weight the scenarios explicitly:

- Base case (central assumptions): 40 percent probability

- Upside (faster revenue ramp, margin expansion, higher exit multiple): 25 percent

- Downside (slower ramp, margin compression, multiple compression): 25 percent

- Failure (company does not reach terminal year, or terminal year is reached at a fraction of projected revenue): 10 percent

The probability-weighted intrinsic value is the number we compare to the current price. A model that assigns zero probability to the failure case for a pre-profit startup is not a model — it is a pitch deck. The failure scenario has to carry real weight, and the position size has to survive a total loss. When you strip away the precision of the spreadsheet, what remains is a structured bet: you are buying a probability distribution, not a stock.

When terminal value dominates, the model is a probability machine. The output is expected value across scenarios, not a price target.

Cross-Validating DCF Results with Revenue-Based Multiples

Price-to-earnings is structurally unusable for a company with negative net income. The standard cross-check is EV/Revenue and EV/EBITDA applied to the projected financials from the explicit forecast period — typically year five or year seven numbers that already sit inside the model.

The check answers a direct question: at the valuation implied by our DCF, what forward multiple is the market paying for those projected fundamentals? If the DCF says the company is worth $1B and year-five revenue is projected at $200M, the implied forward EV/Revenue is 5x at year five or 50x on current revenue. Neither number is useful in isolation. The relevant comparison is the implied multiple versus the comparable set at the same growth stage and margin profile.

If mature peers in the same vertical trade at 8 to 12x EV/Revenue and our model implies 15x at year five, we need a specific, testable reason for the premium — faster revenue growth, higher net retention, a defensible cost advantage. Generic appeals to "disruption" or "market opportunity" are not reasons. The premium must be quantified and matched to an observable operating metric that can be tracked over time.

We also reconcile against EV/EBITDA once projected EBITDA turns positive. If the DCF implies 35x EV/EBITDA on year-seven numbers and peers trade at 18x, either the growth differential justifies the premium or the exit multiple assumption embedded in the terminal value calculation is too generous. The two cross-checks — revenue-based and earnings-based — should tell a consistent story. When they diverge, the analyst has to identify which assumption is carrying the excess weight and determine whether that assumption is anchored to evidence or to conviction.

Position Sizing and Portfolio Integration

The DCF output is one input in a broader decision framework. For negative-earnings startups, position sizing and exit discipline carry as much analytical weight as the valuation itself — sometimes more, because the valuation range is wide enough that the size of the position determines the actual risk exposure more than the center of the range.

We cap venture-stage positions so that a total-loss outcome does not breach the portfolio's maximum drawdown tolerance for high-risk allocation. If the portfolio allocates 15 percent to venture-stage exposure, no single pre-profit name commands more than 2 to 3 percent at entry. This is not a risk management afterthought — it is a structural feature of the investment process that allows the model's probability-weighted output to actually play out across a portfolio of positions rather than being consumed by a single catastrophic loss.

The discount rate should be anchored to a documented failure probability, not a generic venture-stage premium. The normalized margin should trace to a named comparable set where both the median and the range are visible. The exit multiple should sit below current peer levels to embed conservatism into the terminal value. And the holding period assumption should be explicit: we do not assume the model plays out on the labeled timeline. A position that cannot exit on the modeled schedule carries a different risk profile than the one the model priced — illiquidity is a cost, and it compounds.

Liquidity constraints also matter at the portfolio level. Secondary market marks are not primary valuations, and a position that is locked up for three years requires a different sizing framework than one that can be exited at will. We account for this through the overall liquidity budget rather than through a discount applied to a single holding — it is a portfolio construction problem, not an asset pricing problem.

A DCF for a pre-profit company that produces a single number is a DCF that has failed its purpose. The honest output is a probability-weighted range, a documented set of assumptions, and a clear-eyed assessment of which parameters the thesis depends on most heavily. Build the model to be challenged, not to be believed — because the market will do the challenging for you, and the only question is whether you identified the pressure points before the price did.