Compare Analyst Price Targets to Find Value Stocks

A stock trading 28% below its consensus price target is not automatically cheap. It is only trading below the arithmetic average of several analyst models, most of which use different assumptions…

A stock trading 28% below its consensus price target is not automatically cheap. It is only trading below the arithmetic average of several analyst models, most of which use different assumptions, different terminal multiples, and the same convenient 12-month horizon. That gap may signal undervaluation. It may also signal stale estimates, margin deterioration, deteriorating cash conversion, or a balance sheet problem the target price has not yet absorbed.

This is the first error in learning how to check compare analyst price targets to find value stocks: treating the consensus target as a substitute for valuation. It is not. A price target is an opinion with a timestamp. Intrinsic value is a claim on future cash flows, adjusted for risk, reinvestment, dilution, debt, and accounting quality. The two can overlap. Often, they merely nod at each other from opposite sides of a spreadsheet.

Decoding the 12-Month Horizon

Most analyst price targets are 12-month forward-looking estimates. That sounds precise. It is not. It is a convention.

The 12-month frame creates a strange hybrid. It is too long to be a trading signal and too short to be a full intrinsic value estimate. Analysts are asked to compress a company’s strategic, cyclical, and accounting reality into a one-year destination price. The result is a number that often reflects expected earnings revisions, valuation multiple expansion, and market sentiment as much as underlying business value.

A target price usually comes from one of several valuation methods:

- a forward earnings multiple applied to estimated EPS;

- an enterprise value multiple applied to EBITDA, revenue, or free cash flow;

- a discounted cash flow model;

- a sum-of-the-parts calculation;

- a sector-relative valuation framework.

Each method has its own failure mode. EPS multiples can ignore stock-based compensation and capitalized costs. EBITDA multiples can flatter companies with heavy maintenance capex. Revenue multiples can excuse poor unit economics. DCF models can hide almost any conclusion in the terminal value. Sum-of-the-parts analysis can become a polite way to overvalue every segment separately.

The investor comparing analyst price targets is therefore not comparing facts. He is comparing model outputs. That distinction matters.

A consensus target is not a scale. It is a collection of calibrated opinions, some fresh, some stale, some still carrying last quarter’s assumptions.

For a value screen, the 12-month target should be used as a starting anomaly. It asks a useful question: why does the analyst community think the stock is worth more than the market price? It does not answer whether the market is wrong.

The correct sequence is blunt:

1. Identify the current price and consensus target.

2. Calculate the implied upside.

3. Examine the spread between individual targets.

4. Check the rating distribution.

5. Compare the implied valuation to fundamentals.

6. Remove companies where the accounting does not support the thesis.

The last step does most of the work. It is also the step most screeners skip.

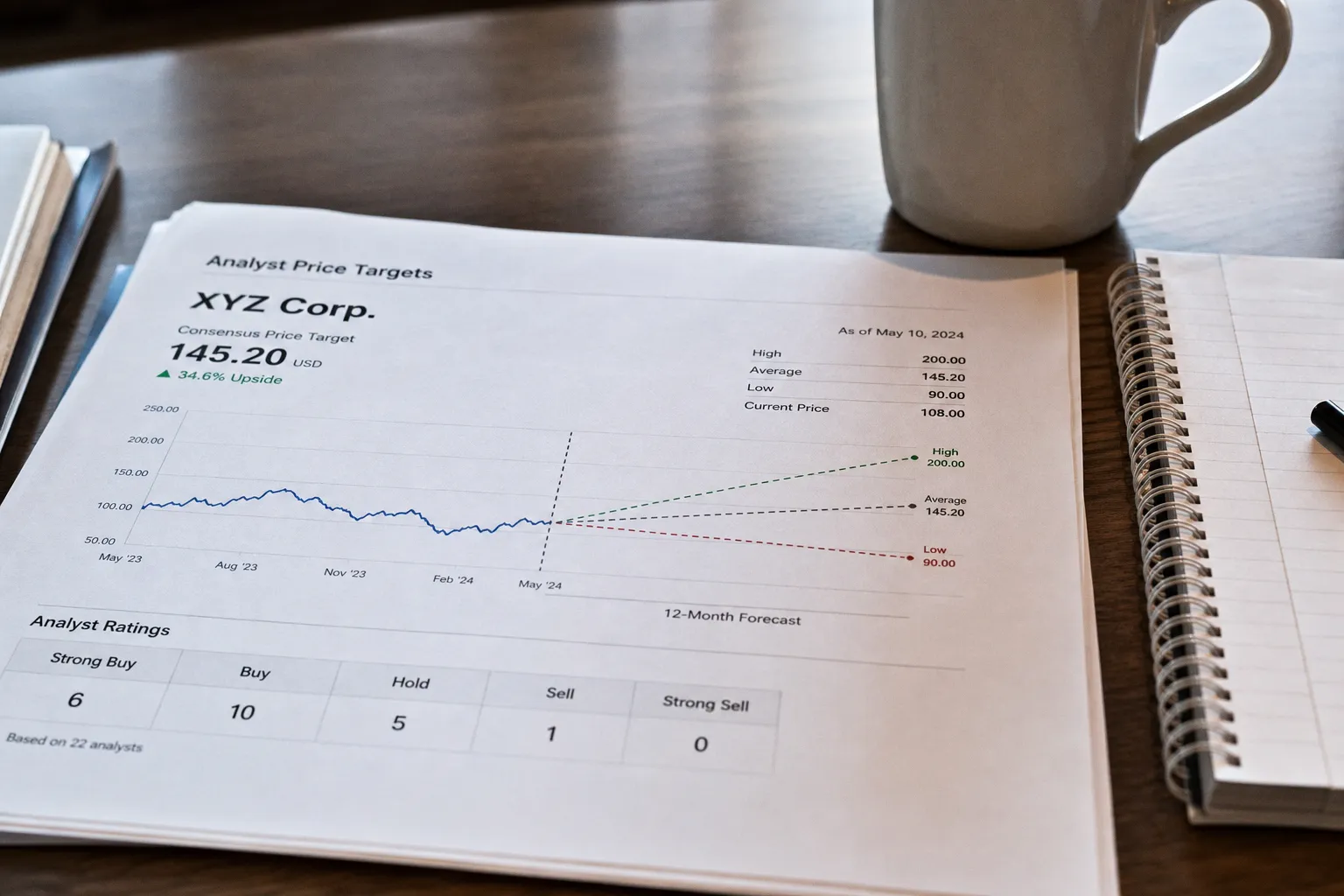

Calculating Upside Potential and Consensus Variance

The basic formula is simple:

Upside potential = (Consensus Price Target - Current Price) / Current Price

If a stock trades at $40 and the consensus target is $52, the implied upside is 30%. That looks useful. It is incomplete.

A 30% upside based on 20 analysts with tight estimates is not the same as a 30% upside based on three analysts whose targets range from $25 to $80. The arithmetic mean hides the quality of the signal.

The investor should separate three numbers:

| Measure | What it shows | Why it matters |

|---|---|---|

| Current price | The market’s current clearing price | This is the only hard market number in the exercise |

| Consensus target | Mean of individual analyst targets | Useful, but vulnerable to outliers and stale models |

| Target dispersion | Range or standard deviation of targets | Measures disagreement and model fragility |

| Median target | Middle estimate | Often cleaner than the mean when outliers distort consensus |

| Implied upside | Gap between target and price | A screening input, not a valuation conclusion |

The dispersion is the first forensic test. If the average target is high because one optimistic analyst carries an extreme estimate, the consensus is not a consensus. It is arithmetic contamination.

A clean comparison should include the highest target, lowest target, mean target, and median target. If the mean and median sit close together, the group view is more coherent. If the mean sits materially above the median, one or two aggressive targets may be inflating the headline upside.

There is a practical way to classify the signal:

- Low upside, low dispersion: usually fairly priced or already understood.

- High upside, low dispersion: worth investigating; the market may be discounting a risk analysts think is temporary.

- High upside, high dispersion: unstable signal; valuation depends heavily on contested assumptions.

- Low upside, high dispersion: little margin for error and poor agreement; usually not a value setup.

The third category is where many traps live. A stock can show 45% upside because half the analyst group assumes margin recovery while the other half assumes permanent impairment. The consensus target splits the difference and produces a number that looks scientific. It is not.

The Staleness Problem

Consensus data also decays. If a company reports weak earnings, lowers guidance, or shows a working capital reversal, the current stock price adjusts immediately. Analyst targets may not. Some analysts update within hours. Others wait for a full model refresh. During that lag, the “upside” can expand mechanically.

This is common after earnings disappointments. The price falls. The target remains unchanged. The screener then flags the stock as undervalued. In reality, the numerator is stale.

A disciplined investor checks whether recent price action was driven by new information:

- revenue miss;

- gross margin compression;

- operating deleverage;

- higher interest expense;

- inventory build;

- receivables growth above sales growth;

- management guidance cut;

- impairment charge;

- covenant pressure;

- capital raise or dilution.

If the target has not absorbed those facts, the upside calculation is an accounting fossil.

Identifying Optimism Bias in Equity Research

Analyst price targets often exhibit optimism bias. This is not a moral claim. It is a structural observation.

Equity research sits inside a market ecosystem that usually rewards access, coverage, and constructive framing more than persistent negativity. Sell ratings are rarer than buy or hold ratings. Price targets often lean above the current price, particularly in rising markets or for companies with popular growth narratives.

This does not make analyst work useless. It means the investor must haircut it.

A sober comparison starts by adjusting the consensus target down before treating it as a value clue. The haircut does not need false precision. It should reflect the company’s sector, volatility, historical miss pattern, and accounting quality.

A practical framework:

| Condition | Treatment of consensus target |

|---|---|

| Stable earnings, clean cash conversion, low leverage | Small haircut |

| Cyclical revenue, margin volatility, commodity exposure | Moderate haircut |

| Negative free cash flow, heavy stock compensation, repeated guidance cuts | Large haircut |

| Recent impairment, refinancing risk, deteriorating working capital | Treat consensus as suspect |

| Few analysts and wide target spread | Prefer median; discount the mean |

The point is not to punish analysts. It is to remove the default optimism embedded in the published number.

A stock trading 25% below consensus may offer no margin of safety after adjustment. If the realistic target is 10% lower than the published consensus, and another 10% should be removed for execution risk, the apparent bargain nearly disappears. This is basic arithmetic. It is also why headline upside tables are often expensive entertainment.

Investors used to yield screens in other markets, such as staking dashboards or DeFi income tools, may recognize the same issue: the displayed number is only the first layer. The durable question is how the yield, or in equities the target, is generated. The same skepticism applies when reviewing DeFi yield farming and staking mechanics outside public equities.

Distinguishing Between Value Traps and True Undervaluation

A value stock is not merely a stock with upside to a target price. It is a security trading below a reasonable estimate of intrinsic value, with enough balance sheet durability and cash generation to close the gap over time.

A value trap looks similar at first. It trades below consensus. It screens cheap on earnings. It may have several buy ratings. Then the underlying economics deteriorate faster than the multiple can rerate.

The separation begins with accounting.

Cash Conversion

Earnings that do not convert into cash deserve suspicion. If net income rises while operating cash flow lags, the investor should inspect accruals. The common culprits are familiar:

- receivables growing faster than revenue;

- inventory accumulation ahead of weak demand;

- capitalized software or development costs flattering operating profit;

- restructuring charges recurring with impressive regularity;

- stock-based compensation excluded from “adjusted” earnings;

- supplier financing distorting operating cash flow;

- aggressive revenue recognition.

Analyst targets often use adjusted EPS or adjusted EBITDA. Those measures may be reasonable in specific cases. They may also remove the cost of doing business and call the remainder earnings.

A company with poor cash conversion can still receive a high target if the analyst expects normalization. That expectation must be tested. If working capital has consumed cash for several periods, normalization is not a thesis. It is a wish with a spreadsheet tab.

Balance Sheet Risk

A cheap multiple can be a debt problem wearing a value costume.

The equity value of a leveraged company can move violently because small changes in enterprise value flow disproportionately to shareholders. Analyst targets may appear attractive during cyclical downturns because the model assumes recovery before liquidity becomes urgent. The market may be pricing the debt wall instead.

For leveraged companies, comparing price targets without looking at maturities, interest coverage, and refinancing terms is incomplete. Higher rates can turn a low P/E stock into a declining equity stub. If interest expense absorbs operating improvement, the upside belongs to creditors first.

The investor should examine:

1. Net debt relative to EBITDA, using normalized EBITDA rather than peak EBITDA.

2. Interest coverage after maintenance capex, not just EBIT.

3. Debt maturities over the next three years.

4. Covenant headroom if earnings fall again.

5. Pension obligations, lease liabilities, and off-balance-sheet commitments where relevant.

Analysts may discuss these items. The target price, however, often compresses them into a risk premium. That compression can be too gentle.

Impairment and Capitalized Costs

Impairments are accounting admissions. They tell the investor that capital previously recorded as productive is no longer worth its carrying value. A one-time impairment can be a reset. Repeated impairments are evidence of poor capital allocation.

Capitalized costs deserve similar attention. When companies capitalize expenses, current earnings improve while assets build on the balance sheet. This is not automatically aggressive. Software development, content costs, and long-term project costs can be legitimately capitalized. But the pattern matters.

If capitalized costs rise faster than revenue, and amortization trails the economic consumption of those assets, reported margins can overstate economic margins. Analyst targets based on those margins will be too high.

The value trap usually announces itself in the cash flow statement before it confesses in the income statement.

Integrating Rating Distributions Into Fundamental Analysis

Buy, Hold, and Sell ratings are useful only when read as distribution, not as labels. A stock with 80% Buy ratings and 20% Hold ratings may seem stronger than one with a mixed profile. But the distribution must be matched to valuation, estimate revisions, and price target dispersion.

A crowded Buy rating can mean confidence. It can also mean expectations are already embedded. If a stock has many Buy ratings, a high consensus target, and demanding earnings assumptions, the burden of proof shifts to execution. Any miss can cause multiple compression.

A mixed rating distribution can be more interesting. If several analysts are cautious but the balance sheet is clean, free cash flow is improving, and pessimistic assumptions are already reflected in the price, disagreement may create opportunity.

The investor should read rating distribution through four lenses:

- Concentration: Are most analysts clustered around Buy, or is there real disagreement?

- Direction of change: Are upgrades increasing after estimate revisions, or are analysts defending old targets?

- Target movement: Are targets rising because earnings estimates are rising, or because multiples are expanding?

- Valuation bridge: Does the target depend on better cash flow, higher margins, lower discount rates, or simple optimism?

The last point is central. A price target should be decomposed. If an analyst assigns a $60 target to a stock trading at $45, the investor should ask what gets the stock from $45 to $60. There are only a few levers:

1. Earnings estimates rise.

2. The valuation multiple expands.

3. Free cash flow improves.

4. Debt declines.

5. Capital returns increase.

6. Segment valuation changes.

7. Market risk appetite improves.

Some levers are operational. Some are financial. Some are just mood. The market pays differently for each.

A Worked Comparison

Consider two hypothetical stocks. Both trade 30% below consensus target. A basic screener treats them as similar. They are not.

| Parameter | Stock A | Stock B |

|---|---|---|

| Current price | $50 | $50 |

| Consensus target | $65 | $65 |

| Implied upside | 30% | 30% |

| Target range | $60–$70 | $38–$92 |

| Median target | $64 | $58 |

| Rating distribution | 70% Buy, 30% Hold | 40% Buy, 50% Hold, 10% Sell |

| Free cash flow trend | Positive and rising | Negative for three periods |

| Net debt | Low | High |

| Recent revisions | EPS estimates up | Revenue and margin estimates down |

| Working capital | Stable | Inventory rising faster than sales |

Stock A may deserve further work. The targets are clustered. The median supports the mean. Cash flow is improving. Estimate revisions confirm the direction.

Stock B is not a value stock because the upside column says 30%. It is a contested situation with poor cash conversion, leverage, and wide model disagreement. The consensus target is averaging incompatible views. That is not analysis. It is arithmetic camouflage.

Building a Price Target Comparison Process

The process should be mechanical enough to avoid narrative drift and flexible enough to catch accounting distortions. The purpose is not to outsource valuation to analysts. It is to use their work as a map of market expectations.

A disciplined workflow looks like this:

1. Start with the consensus gap. Screen for stocks trading materially below consensus target. Do not rank them by upside alone.

2. Check analyst count. A consensus based on two analysts carries little weight. A larger group can still be wrong, but at least the average has breadth.

3. Compare mean and median targets. If the mean is meaningfully higher than the median, isolate the outlier targets.

4. Measure target dispersion. Wide dispersion means the business model, cycle, or balance sheet is difficult to underwrite.

5. Review rating distribution. Look for disagreement, recent changes, and whether Buy ratings are being maintained despite estimate cuts.

6. Inspect revisions. A target that stays flat while earnings estimates fall is suspect unless the multiple assumption is explicitly changing for a defensible reason.

7. Rebuild the implied valuation. Convert the target into P/E, EV/EBITDA, price/free cash flow, or DCF assumptions. See what must be true.

8. Test cash quality. Compare earnings to operating cash flow and free cash flow. Follow accruals.

9. Check leverage and dilution. Upside to equity can vanish through refinancing, share issuance, or rising interest expense.

10. Apply an optimism haircut. Adjust the target for bias, cyclicality, and accounting risk before calling the stock undervalued.

This process will reject many apparent bargains. That is a feature.

A useful value screen should produce fewer names after each step. If the list does not shrink, the process is not discriminating. It is decorating the original screen.

From Price Target to Intrinsic Value

The final step is to stop looking at the target and build a valuation.

Analyst targets can indicate where the market debate sits. They cannot determine what the business is worth. Intrinsic value requires assumptions about normalized earnings power, reinvestment needs, competitive position, capital intensity, tax rate, financing cost, and shareholder dilution.

For a mature company, the investor can triangulate value using normalized free cash flow. For a cyclical company, mid-cycle margins matter more than current margins. For a growth company, the question is whether incremental revenue converts into durable cash flow or merely absorbs capital through working capital, sales expense, and stock compensation.

The target price comparison should feed into valuation this way:

| Question | Use of analyst targets | Independent valuation test |

|---|---|---|

| Is the market pricing pessimism? | Compare current price to consensus and median targets | Examine normalized margins and free cash flow |

| Is there analyst agreement? | Review target dispersion and rating distribution | Test whether assumptions converge around realistic fundamentals |

| Is upside driven by earnings or multiple expansion? | Reverse-engineer target multiples | Compare to sector history and return on invested capital |

| Is the stock cheap or impaired? | Note target gap after recent selloff | Inspect cash conversion, leverage, and impairments |

| Is the thesis time-sensitive? | Check 12-month catalyst assumptions | Determine whether intrinsic value depends on near-term sentiment |

The last distinction is often ignored. A price target usually needs a path within 12 months. Intrinsic value does not always need that path immediately. A stock can be undervalued with no near-term catalyst. It can also have a near-term catalyst and still be overvalued.

Value investors should care more about downside protection than target convergence. A stock with 20% upside and limited downside may be superior to one with 60% upside and a capital structure that can dilute shareholders if the cycle turns.

The Sober Use of Consensus

The clean use of analyst price targets is not to believe them. It is to interrogate them.

A large gap between market price and consensus target identifies tension. That tension may come from market overreaction, delayed analyst revisions, structural decline, or an accounting issue hiding beneath adjusted earnings. Only one of those is attractive.

The investor looking for value should prefer situations where the target gap is supported by clustered estimates, improving revisions, clean cash conversion, manageable leverage, and a valuation that still works after an optimism haircut. Everything else belongs in the watchlist, not the portfolio.

A reasonable intrinsic value estimate should be built below the published consensus, not above it. If the stock still offers adequate upside after that discount, the opportunity may be real. If the margin of safety disappears once stale targets, aggressive multiples, and weak cash flow are removed, the market was not irrational. It was simply faster than the spreadsheet.

FAQ

Why is a stock trading below its consensus price target not necessarily a bargain?

What does a high target dispersion mean for an investor?

How can I tell if a stock is a value trap rather than truly undervalued?

Why do analyst price targets often exhibit optimism bias?

What is the problem with the 12-month horizon used in price targets?

By Russell Cobb